Wednesday, May 21, 2014

How Quickly Homes are Selling 2013 v. 2014

Through April, the number of days required to get a home sold depends on where the home is located

Tuesday, May 20, 2014

FSBO Millionaires Use Real Estate Agents

They are happy to take money encouraging others to try to sell their own homes. However, when it comes time to sell their own home, it's do as I say not as I do:

FSBO Millionaires Use Real Estate Agents

FSBO Millionaires Use Real Estate Agents

Monday, May 19, 2014

Friday, May 16, 2014

Price Changes since last year

As always, real estate is local. Cumberland county is up nicely from last year while Dauphin is down slightly

Wednesday, May 14, 2014

Lawn Biker Breakfast is This Sunday

In my opinion this is the best of the biker breakfasts in Central PA.

As many as 1500 bikes and great food.

As many as 1500 bikes and great food.

Lawn Fire Company & Ambulance

5596 Elizabethtown Road

Lawn, PA 17041

Sunday 7-11

Monday, May 12, 2014

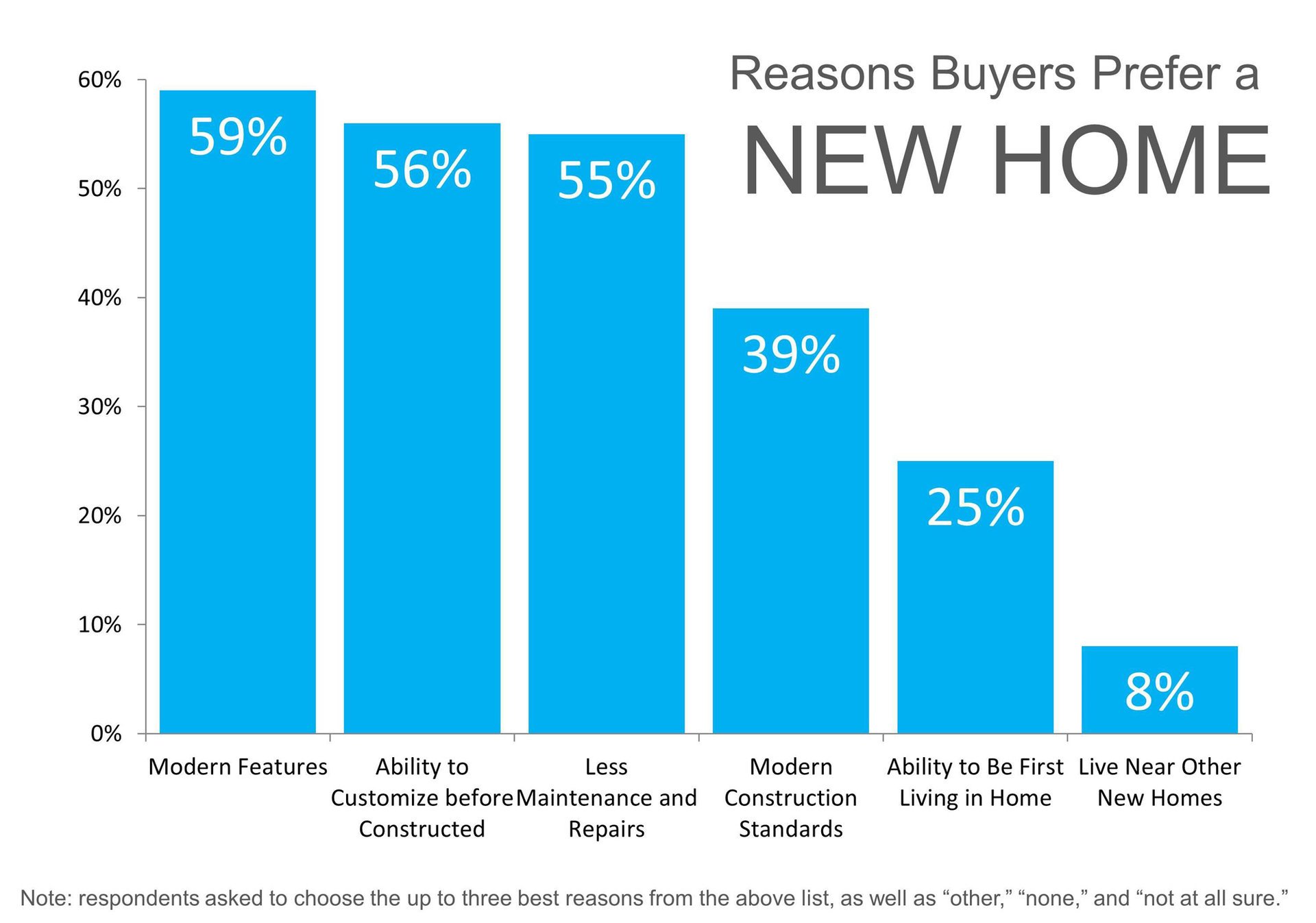

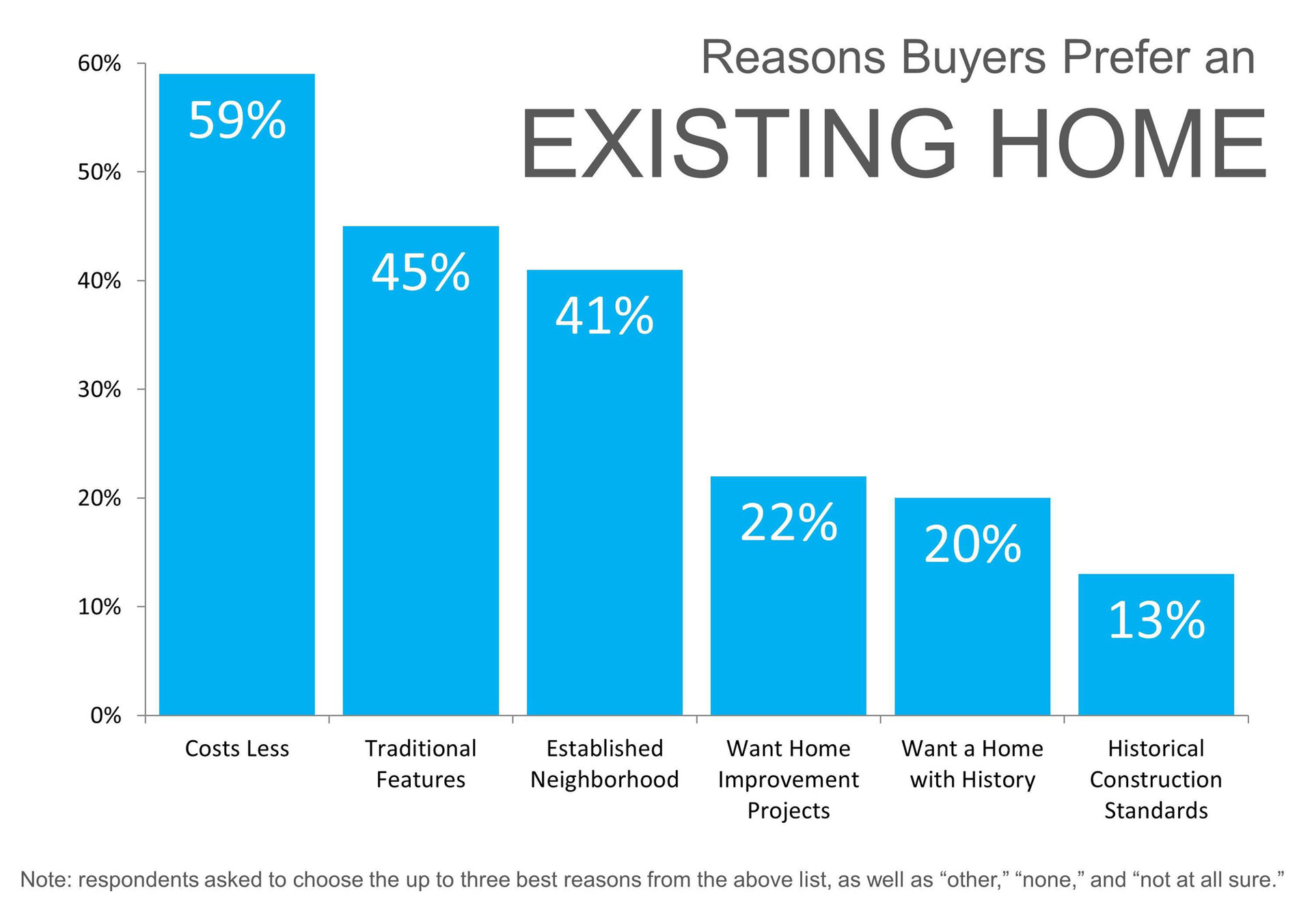

Buyers prefer new but are they willing to pay?

41% of Americans Would Prefer to Build their Home

A recent study by Harris Poll revealed that, for the same price, forty one percent of Americans would prefer to buy a newly built home instead of an existing home. Twenty one percent prefer an existing home while thirty eight percent didn’t have a preference.

*Trulia estimates “that new homes built in 2013 or 2014 are typically priced 20 percent higher than older homes of a similar size and location.”

Why People Prefer a New Home?

Why People Prefer an Existing Home?

Friday, May 9, 2014

Harrisburg PA area Real Estate Stats

With 6 months supply being generally accepted as a balanced market the current market seems to favor buyers in all price ranges in both Cumberland and Dauphin Counties

Tuesday, May 6, 2014

Sometimes even the Wall StreetJournal misses

Homeownership: This Time the Wall Street Journal Got it Wrong

Our founder, Steve Harney, occasionally asks to do a personal post on what he sees as important to our industry. Today is one of those days. Enjoy! – The KCM Crew

I have been a subscriber to the Wall Street Journal (WSJ) for as long as I can remember. In my opinion, it is the single greatest source of financial information and insights available. I don’t always agree with their analysis but I always respect their position.

I have been a subscriber to the Wall Street Journal (WSJ) for as long as I can remember. In my opinion, it is the single greatest source of financial information and insights available. I don’t always agree with their analysis but I always respect their position.

However, in an article this past weekend,The New Math of Renting vs. Buying, they flat out got it wrong. Below are a few excerpts from the article and the reason why I believe the analysis to be incorrect.

The Cost of Renting is Lower than the Cost of Owning

In the article, they discuss that homeownership is more expensive than renting in many large metropolitan areas.

"The monthly cost of renting was lower than buying in 20 large metropolitan areas at the end of last year, the most recent period for which data are available, according to figures provided exclusively to The Wall Street Journal by Deutsche Bank. That is up from 15 large metropolitan areas a year earlier.”

The challenge is that more recent data from two very reliable sources has shown that not to be the case. Among the 35 largest metro areas analyzed by Zillow in the first quarter, every metro showed it would be cheaper to buy than rent if you plan to live in the home for at least 4.2 years.

According to a study by Trulia:

“Homeownership remains cheaper than renting nationally and in all of the 100 largest metro areas. Rising mortgage rates and home prices have narrowed the gap over the past year, though rates have recently dropped and price gains are slowing. Now, at a 30-year fixed rate of 4.5%, buying is 38% cheaper than renting nationally.” (emphasis added)

Renters Don’t Have All the Expenses of Homeowners

The article goes on to explain that as a renter you have many less expenses than you would have as a homeowner:

"Renters, for example, don't pay property taxes, homeowner's insurance and, in most cases, maintenance costs. These expenses can cost homeowners about 3% of the price of their home annually, experts say.

While those costs can be folded into monthly rent, apartment renters often pay a smaller share as landlords spread the costs among many tenants, says Stijn Van Nieuwerburgh, director of the Center for Real Estate Finance Research at New York University. If a window breaks or the toilet plugs up, your landlord—not you—pays for the repairs."

Don’t kid yourself – the landlord does not pay the taxes nor pay for repairs. The tenant does. It is incorporated in the rent. It is true, if it is an apartment building, that the property taxes are shared by all tenants. However, realize that the amount of property taxes for an apartment building with “many tenants” will be far greater than a single family residence.

We think this situation is best explained by Eric Belsky, Managing Director of the Joint Center of Housing Studies at Harvard University, in his paper on homeownership - The Dream Lives On: the Future of Homeownership in America:

“Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return. That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.” (emphasis is mine)

Investing the Difference in Payments Will Net a Renter More Money

The WSJ article claims that, if a renter invests the difference between their rent payment and a potential mortgage payment had they purchased, they would be better off financially in the long run.

"Renters don't end up with a valuable asset, as buyers do when they pay off a mortgage. But renters might be able to make more money by investing the monthly savings, as well as the cash they would otherwise use for a down payment, he says."

They go on to explain their reasoning as follows:

"The value of the average single-family home increased by 3.6% a year in the three decades through 2013, compounded annually, according to mortgage giant Freddie Mac. By contrast, the compound annual return on the S&P 500 over that period was 11.1%, according to Chicago-based investment-research firm Morningstar."

As to the idea that the return on investment would be greater by investing in the stock market rather than purchase a home, I think the article in the WSJ forgot that housing is a leveraged investment. Belsky, in his paper, explains:

“Few households are interested in borrowing money to buy stocks and bonds and few lenders are willing to lend them the money. As a result, homeownership allows households to amplify any appreciation on the value of their homes by a leverage factor. Even a hefty 20 percent down payment results in a leverage factor of five so that every percentage point rise in the value of the home is a 5 percent return on their equity. With many buyers putting 10 percent or less down, their leverage factor is 10 or more.”

That 3.6% average annual appreciation is really an 18% return on cash to a home buyer putting down 20%.

They also assume the renter will save any difference in housing expense. However, that does not happen in reality. In their ongoing research for their paper, Beer and Cookies Impact on Homeowners’ Wealth Accumulation, Eli Beracha and Ken H. Johnson reveal that homeownership creates a ‘forced savings’ plan:

“It appears that homeownership creates extra wealth mainly through its ability to force owners to save rather than through property appreciation. Thus, homeownership appears to be a self-imposed savings plan, which through time leads to greater wealth accumulation as compared to comparable renters. In short, buying a home makes Americans save.”

And Belsky from Harvard agrees:

“Since many people have trouble saving and have to make a housing payment one way or the other, owning a home can overcome people’s tendency to defer savings to another day.”

To further make this point, we can look at a study by the Federal Reserve which showed that the net worth of a homeowner ($174,500) is 30 times greater than that of renter ($5,100).

Bottom Line

Looking at financial advantages of homeownership from every angle still reveals that it is a much better investment than renting.

Friday, May 2, 2014

Weekend Projects

5 Easy DIY Weekend Projects Under $300

Published: May 24, 2012

Just another weekend? Not if you take advantage with one or more of these 5 great projects you can easily pull off for under $300.

Most of the cost of these DIY weekend projects is in the materials. The labor — that’s you — is free. All you need now are the hours. But, hey, you’ve got two full days — plenty of time to be a superhero weekend warrior and grab some R&R.

Project #1: Add a garden arbor entry.

The setup: Install an eye-catching portal to your garden with a freestanding arbor. It’ll look great at the end of a garden path or framing a grassy area between planting beds.

Specs and cost: Garden arbors can be priced up to thousands of dollars, but you can find nice-looking kits in redwood, cedar, and vinyl at your local home improvement or garden center for $200-$300. Typical sizes are about 7 feet high and 3-4 feet wide. You’ll have to assemble the kit yourself.

Tools: Screwdriver; cordless drill/driver; hammer; tape measure. Kits come pre-cut and pre-drilled for easy assembly, and usually include screws. If fasteners aren’t included, check the materials list before you leave the store.

Time: 3-5 hours

Project #2: Install a window awning.

The setup: Summer is super, but too much sunlight from south- and west-facing windows can heat up your interiors and make your AC work overtime. Beat that heat and save energy by using an awning to stop harsh sunlight before it enters your house.

Specs and cost: Residential awnings come in many sizes and colors. Some are plastic or aluminum, but most are made with weatherproof fabrics. They’re engineered for wind resistance, and some are retractable. A 4-foot-wide awning with a 2.5-foot projection is $150-$250.

Tools: Cordless drill/driver; adjustable wrench; tape measure; level. You can install an awning on any siding surface, but you’ll need a hammer drill to drill holes in brick. To prevent leaks, fill any drilled holes with silicone sealant before you install screws and bolts.

Time: 3-4 hours

How-to video

Project # 3: Screen off your air conditioner from view.

The setup: Air conditioning is great, but air conditioner condensers are ugly. Up your curb appeal quotient by hiding your AC condenser or heat pump unit with a simple screen.

Specs and costs: An AC screen is typically 3-sided, about 40 inches high, and freestanding — you’ll want to be able to move it easily when it comes time to service your HVAC. For about $100, you can make a screen yourself using weather-resistant cedar or pressure-treated wood to build 3 frames, and filling each frame with plastic or pressure-treated lattice.

Or, buy pre-made fencing panels. A 38-by-38-inch plastic fencing panel is about $50.

Tools: Hammer; saw; cordless drill/driver; measuring tape; galvanized wood screws.

Time: Build it yourself in 4-6 hours. Install pre-made fencing in 1-2 hours.

Project # 4: Add garage storage.

The setup: Shopping for garage storage solutions is definitely a kid-in-the-candy-store experience. There are so many cool shelves, hooks, and hangers available that you’ll need to prioritize your needs. Take stock of long-handled landscape tools, bikes, paint supplies, ladders, and odd ducks, such as that kayak. Measure your available space so you’ll have a rough idea of where everything goes.

Specs and cost: Set your under-$300 budget, grab a cart, and get shopping. Many storage systems are made to be hung on drywall, but hooks and heavy items should be fastened directly to studs. Use a stud finder ($20) to locate solid framing.

If your garage is unfinished, add strips of wood horizontally across studs so you’ll have something to fasten your storage goodies to. An 8-foot-long 2-by-4 is about $2.50.

Tools: Cordless drill/driver; hammer; level; measuring tape; screws and nails.

Time: This is a simple project, but not a fast one. Figure 6-10 hours to get everything where you want it, plus shopping. But, oh the fun in putting everything in its place!

Garage storage video

Project #5: Edging your garden.

The setup: Edging is a great way to define your planting beds, corral garden mulch, and to separate your lawn from your garden or patio.

Specs and cost: Wood and metal edging looks like tiny fencing; they’re 4-6 inches high. Some include spikes that hold the edging in position; other types must be partially buried. Cost is $1-$5 per foot.

Plastic edging can be molded and colored to mimic brick, wood, and stone. About $20 for 10 feet.

Concrete edging blocks are smooth, or textured to resemble stone. $15-$25 for 10 feet.

Real stone edging is installed flush with the surrounding grade in a shallow trench on a bed of sand, so digging is required. Stone is sold by the ton and prices vary by region. You’ll need about one-third of a ton of flagstone to make an 8-inch-wide edging 50 feet long, costing $150-$200.

Tools: Shovel; wheelbarrow; tin snips (for cutting plastic edging); work gloves.

Time: Pre-made edging will take 2-3 hours for 50 feet; stone will take 6-10 hours.

Landscape edging video

Read more: http://members.houselogic.com/articles/diy-weekend-projects-for-home/preview/#ixzz30ZUWQhW0

Follow us: @houselogic on Twitter | houselogic on Facebook

Subscribe to:

Comments (Atom)